From One Bubble to the Next

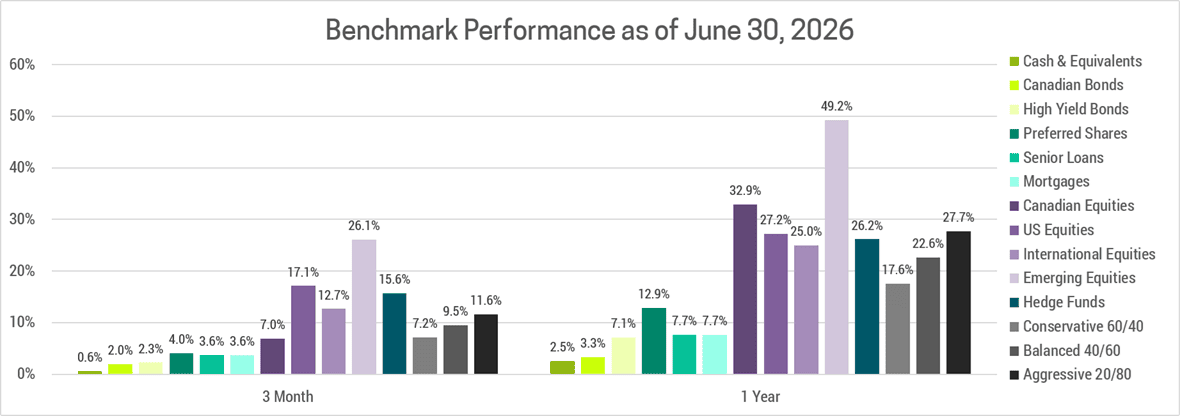

It was yet another strong quarter for investors, as nearly every major asset class was up. The largest gains came from semiconductors, specifically DRAM manufacturers, as the ongoing AI data center build out drove up prices. While our performance was strong, our underweight in semiconductors caused us to underperform our benchmark this quarter, ending our streak of outperformance in recent years. This should prove temporary, as the valuations and expectations for AI companies have become so excessive that underperformance over the long-term is increasingly likely.

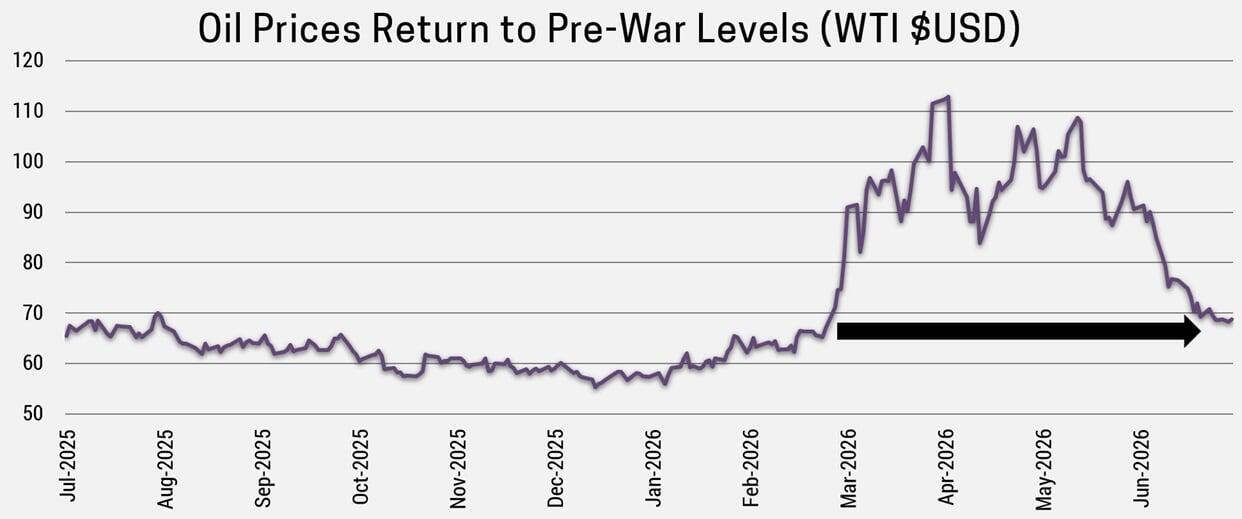

The easing of tensions in the middle east has brought energy prices back to pre-war levels, which should allow the global economy to bounce back. It will take time to rebuild depleted oil inventories, but the markets will look past this so long as a significant re-escalation does not occur.

DE-ESCALATION, NOT RESOLUTION

Central banks are breathing a sigh of relief as falling energy prices should lead to lower inflation. This would reduce the need for interest rate hikes, which has already been reflected in falling bond yields since the fragile ceasefire was announced. Even a short-lived dip in yields will stretch out the economic cycle, even though it will cause long-term problems (more on that later).

We're optimistic in the short-term because the underlying backdrop remains supportive. Monetary and fiscal policy are accommodative (even accounting for the modest rate hikes now priced into markets) and corporate profits are still trending higher. That combination has meant that when markets do sell off, it tends to be a buying opportunity. This will continue until something genuinely breaks the economy's momentum, like a much sharper spike in inflation or interest rates or a bursting of the AI bubble. Negotiations with Iran could still take a turn for the worse, but enough of the parties involved want the Strait to stay open that we view this as a fading risk for now.

FROM ONE BUBBLE TO THE NEXT

All this liquidity from lower than necessary interest rates and burgeoning government deficits doesn’t mean every speculative trade goes on forever. Bitcoin and gold have already seen their bubbles burst, and there's visible stress showing up in parts of the private credit and private equity world. Yet the broader environment for risk assets has stayed positive, which confirms our view that interest rates are too low.

When the cost of capital (borrowing) is lower than the return on capital (growth), money doesn’t leave the system, it just rotates from one hot theme to the next. First, it was the Magnificent 7 mega-cap tech stocks. When those cooled off this spring, investors piled into AI companies, then semiconductor producers. Just last month, money stampeded into the market's newest, hottest IPO, one that promises to literally send investors to the moon, or Mars.

Beyond bubbles, it’s remarkable how resilient this expansion has been. Two wars and their associated energy shocks since 2022, plus last year's trade war, have all failed to knock the global economy off course. If anything, growth looks primed to strengthen further as this latest energy shock fades.

For this backdrop to persist, central banks and governments need room to keep supporting growth rather than being forced into restrictive policy. Some developed-market central banks have begun to implement or talk about rate hikes lately, but the consensus among them is still that inflation will eventually settle back near target, despite having run stubbornly above target for most of this decade. Meanwhile, governments will continue to spend so long as the cost of borrowing remains relatively low.

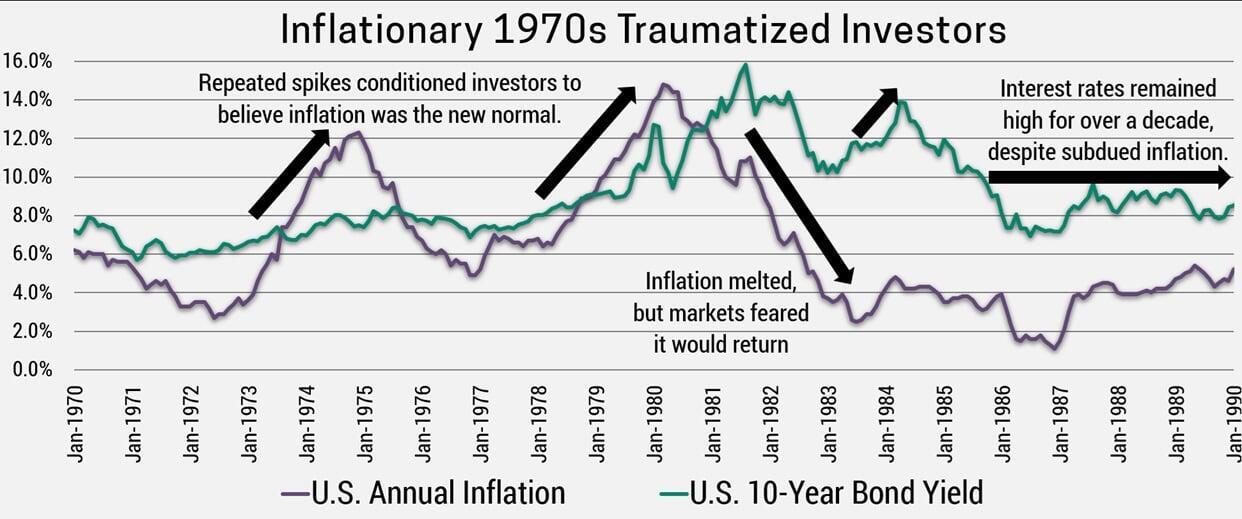

INFLATION RHYMING WITH HISTORY

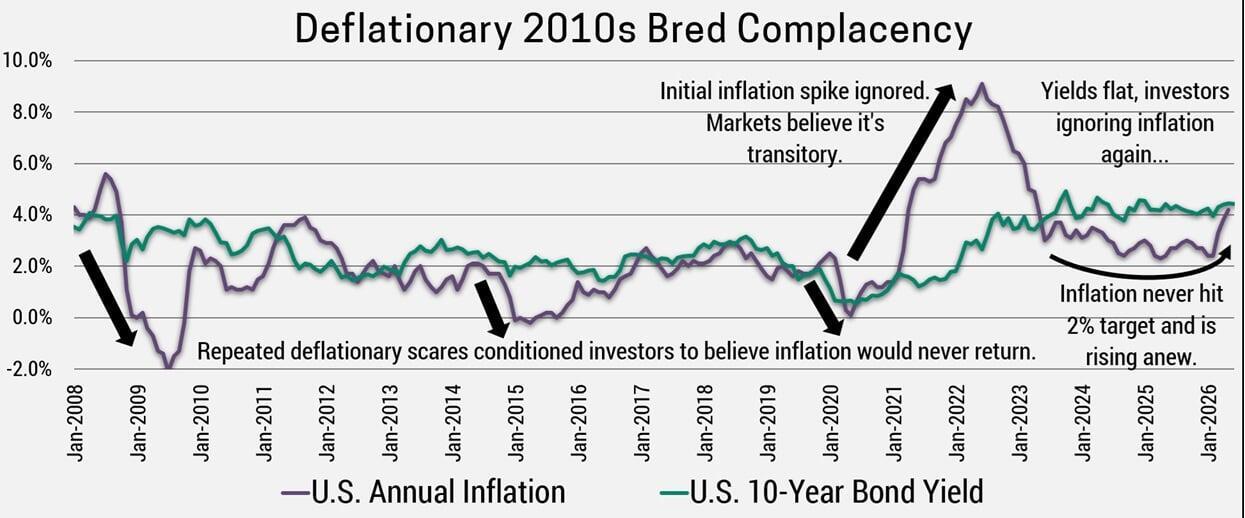

We've written before about how the deflationary decade following the 2008 financial crisis convinced market participants that low inflation was simply the new normal. That belief shaped how policymakers have behaved ever since, and it's part of why we think today's low concern about inflation is misplaced.

Back in the 1980s and 1990s, bond investors (not central banks) were the ones dictating interest rates. Having just lived through the runaway inflation of the 1970s, a group nicknamed the “bond vigilantes” demanded higher yields any time inflation ticked up by selling off government bonds en masse. That kept bond yields persistently above nominal GDP growth (economic growth before adjusting for inflation), which had the effect of keeping a lid on inflation for two full decades, even during periods of strong real growth like the late-1990s.

Then came the 2010s. Having just lived through the 2008 financial crisis, investors and central banks did the mirror opposite: they fought the last war against deflation instead of preparing for the next one against inflation. Bond yields fell below nominal growth and mostly stayed there. A few structural forces reinforced this belief that low inflation was here to stay:

- Limited Wage Growth: Slack in the labour market kept a lid on wages. Since wages are the biggest input cost for most service businesses, it kept service price inflation low.

- Globalization: Companies shifted production to lower-cost countries, which put downward pressure on goods prices.

- Deleveraging: After the 2008 housing bust in the U.S. and the European debt crisis, households and governments spent a decade paying down debt rather than borrowing and spending, which is inherently disinflationary.

Every one of these forces has since gone into reverse. Labour markets have tightened to the point where economic slack has essentially disappeared across developed markets, most notably in the U.S. Globalization has stalled and in some cases reversed, as the pandemic exposed the risks of overseas supply chains and pushed companies toward higher-cost domestic and "friendly" suppliers. And governments have spent the last several years releveraging aggressively through large, persistent deficits rather than paying down debt.

The result is that nominal GDP growth has been running well above bond yields for most of this decade, the opposite of the 1980s-90s bond vigilante era, and much closer to the setup that preceded the inflationary 1970s. Bond investors today simply aren't demanding a premium for inflation risk. This keeps the cost of capital artificially low, which fuels growth that ultimately allows inflation to creep higher.

History doesn't repeat, but it rhymes. It took the Fed the better part of the 1970s and Paul Volcker's brutal rate hikes to finally convince markets inflation was a real threat, and it took two deep recessions to do it. Once that lesson was learned, it stuck around for a generation, right up until the 2010s bred the opposite complacency. We suspect it will take a similarly painful lesson before markets stop assuming today's inflation is simply going to fade quietly on its own.

THE FED KEEPS ITS FOOT ON THE GAS

The Fed is still running an accommodative policy even while inflation stays well above its 2% target, something that's been true for nearly 5 years. The Fed is betting inflation drifts back to 2% without needing to take any real economic risk to make that happen. The new Fed chair, Kevin Warsh, believes productivity gains from AI will allow us to produce more with less, thereby driving down prices and inflation.

We believe it’s premature to draw this conclusion and overly optimistic to assume it will offset all the inflationary forces we’ve already outlined in this newsletter. At best it will take many years for these productivity gains to materialize. In the meantime, AI is proving to be inflationary over the short-term, as it’s driving up the price of semiconductors, energy, materials and labor as a result of the massive data center build out.

Markets recently swung from pricing in rate cuts to pricing in modest hikes, but that looked like a reaction to oil-driven price spikes rather than any real change in the view about inflation as a structural problem. Now that oil has pulled back, both bond yields and rate expectations have eased again. Measures of expected future inflation have cooled too, though notably, they never even rose to a level that would have compensated investors for the inflation actually experienced this decade. The 10-year inflation swap rate, a market gauge of where investors expect inflation to average out over the next decade, is sitting near its lowest level in five years.

THIS DECADE IN TWO WORDS: INFLATION AND PROFITS

If we had to sum up this decade's market environment in two words, they'd be inflation and profits. The two have gone hand-in-hand. Companies have been able to pass along wave after wave of higher costs to customers, which has pushed corporate profit margins to unusually high levels while also keeping consumer inflation elevated. That combination simply wasn't as common in prior decades.

It's become something of a self-reinforcing loop. Higher profits support stronger overall growth, which leaves less slack in the economy and pushes wages up, which allows consumers to keep paying higher prices, which supports even higher profits. At some point this loop breaks, most likely when policymakers are finally forced into a corner or when bond investors decide they've had enough and start demanding higher yields (i.e. a return of the bond vigilante).

Until that happens, investors will keep benefiting from a different kind of inflation: rising asset prices. Individual bubbles pop once investors realize the growth story behind them was never realistic, but the broader liquidity backdrop just sends money chasing the next hot idea, even as overall valuations stay stretched. The eventual endpoint looks fairly clear to us: bond yields will overshoot at some point, because central banks remain growth-focused and are behind the curve on inflation. For now, enjoy the ride, but keep an eye on bond yields and have an exit plan.

PORTFOLIO STRATEGY

We continue to recommend avoiding the hottest, most overvalued pockets of the market, which are running on hype rather than fundamentals. That said, we remain positioned for stocks to outperform bonds overall, and we favour equity sectors and markets outside of expensive U.S. tech, where valuations are far more reasonable. This includes an overweight in international and emerging markets, which were disproportionately affected by the Iran war due to being net energy importers, and now stand to disproportionately benefit from its resolution.

Even as tensions ease, the past few months will leave a lasting mark on supply chains, input costs, and companies' appetite to hold larger inventories as a buffer against the next shock. Like last year's trade war, this energy shock probably won't do serious economic damage on its own, but it adds to a growing pattern of prices becoming more prone to rising over time, a real shift from the low-inflation world of recent decades that we don't think is currently priced into bond markets, or by extension, into asset prices generally. For this reason, we’re positioned for rising bond yields and higher inflation by owning short-term assets like floating rate debt and value stocks.

The short-term outlook has actually improved over the past few weeks. Energy prices are down, supplies through the Strait of Hormuz look set to resume, and bond yields have eased. The healthy pre-war economic outlook is intact and stronger growth looks to be on the way. That growth will likely keep underlying inflation sticky and mildly rising, but central banks show no urgency to take any risks to fight it. We expect the investment backdrop to stay supportive for most risk assets, even as a few of today's hottest trades eventually deflate.