Trump’s War Fuels Higher Inflation

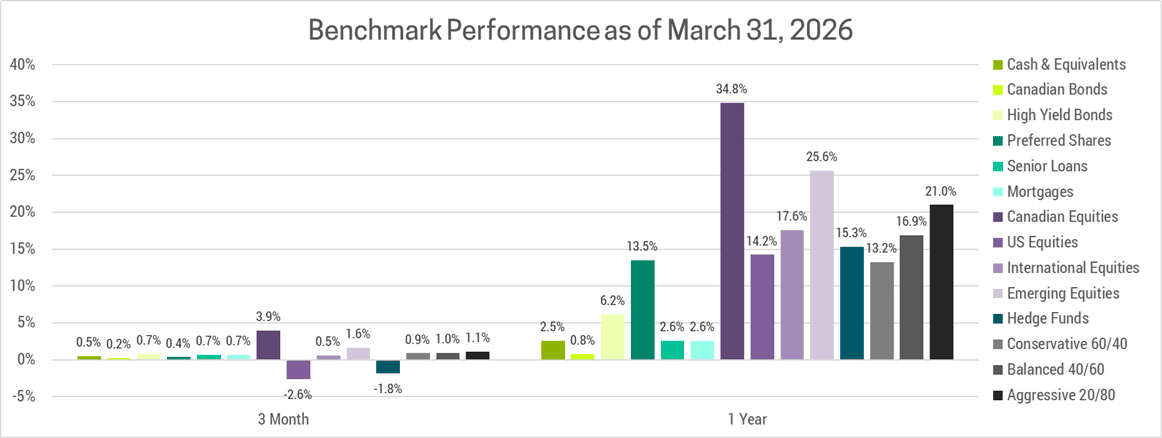

Markets started the year on a high note and continued trending higher until they were derailed by the war in Iran. While the losses in March were a significant setback, they did not fully reverse earlier gains. All major asset classes finished the quarter higher, with the notable exception of U.S. equities. This was not a result of the war, as the U.S. has outperformed other markets since it began. Instead, it was a result of significant underperformance leading up to the war. This has benefited our client portfolios, as we reduced our U.S. equity exposure near their highs early this year, which helped us dramatically outperform our benchmarks once again.

DE-ESCALATION MOST LIKELY

There is a great deal of economic and market uncertainty as a result of the war in Iran. Predicting what happens next is a fool’s errand, but the most likely path forward is de-escalation. Trump, this war, spiking oil prices and inflation are all deeply unpopular at home and with the upcoming mid-term elections the U.S. administration has begun desperately searching for an offramp. Iran is trying to project strength and leverage its control over the Strait of Hormuz, but make no mistake they have suffered economic, military and leadership damage.

It’s unlikely things will return to normal anytime soon. Energy prices in particular are unlikely to return to pre-war levels as there will be a higher embedded risk premium going forward. This is likely to exacerbate already stubborn inflation problems, as energy is an input cost to nearly all goods and services. Even if the Strait of Hormuz is fully reopened, it will take months for global supply chains to recover. Furthermore, there will be a greater risk premium attached to global shipping, which means higher insurance rates and higher prices.

That said, markets don’t care about good or bad, they care about better or worse. The war doesn’t have to be resolved for markets to recover, we just need to be on a path towards de-escalation. When Trump threatens escalation markets sell-off, when he talks about making a deal markets rally. All this happens in the absence of any concrete action, just the intention is enough. Since de-escalation is most likely, we view the recent sell-off as a buying opportunity for long-term investors who can stomach the near-term volatility.

UNCERTAINTY REMAINS ELEVATED

While our base-case assumption is de-escalation, the movement of U.S. troops into the region is concerning. We believe this is posturing in order to secure more favourable terms in ongoing negations, but Trump has proven to be extremely unpredictable. Furthermore, even if the war de-escalates, Iran may not fully reopen the Strait of Hormuz which is the biggest issue for the stock market. This crisis has highlighted the strategic leverage they have over shipping in the region, something they have utilized the shore up massive budgetary shortfalls by charging ships tolls in exchange for safe passage.

These risks are the reason why we have not been rushing in to buy the dip. We are instead being patient and waiting for actions to match the rhetoric. This is primarily because we don’t see enough upside to justify taking the risk of buying too soon. Valuations were elevated going into the crisis and the sell-off has been rather orderly so far. Markets have not experienced a single day of >2% losses since the war broke out. Should the war escalate or drag on longer than expected, markets would suffer more significant losses. If this happens, we would be inclined to buy.

A RESILIENT ECONOMY

The dramatic increase in oil prices has impacted consumer sentiment, but we do not believe it will be sufficient to derail the global economy. We expect the effects to be similar to 2022 when Russia invaded Ukraine. Markets sold off on rising oil prices and concerns it would contribute to a recession, but ultimately the global economy continued to grow (albeit at a slower pace).

The consensus expects oil prices to normalize, as seen in the futures markets, where traders buy and sell oil to be delivered at a future date. Right now, the August 2026 price is below $80 and a year from now is below $70. Should the war and its disruption on energy markets persist longer, this would become a larger drag on growth than is currently perceived.

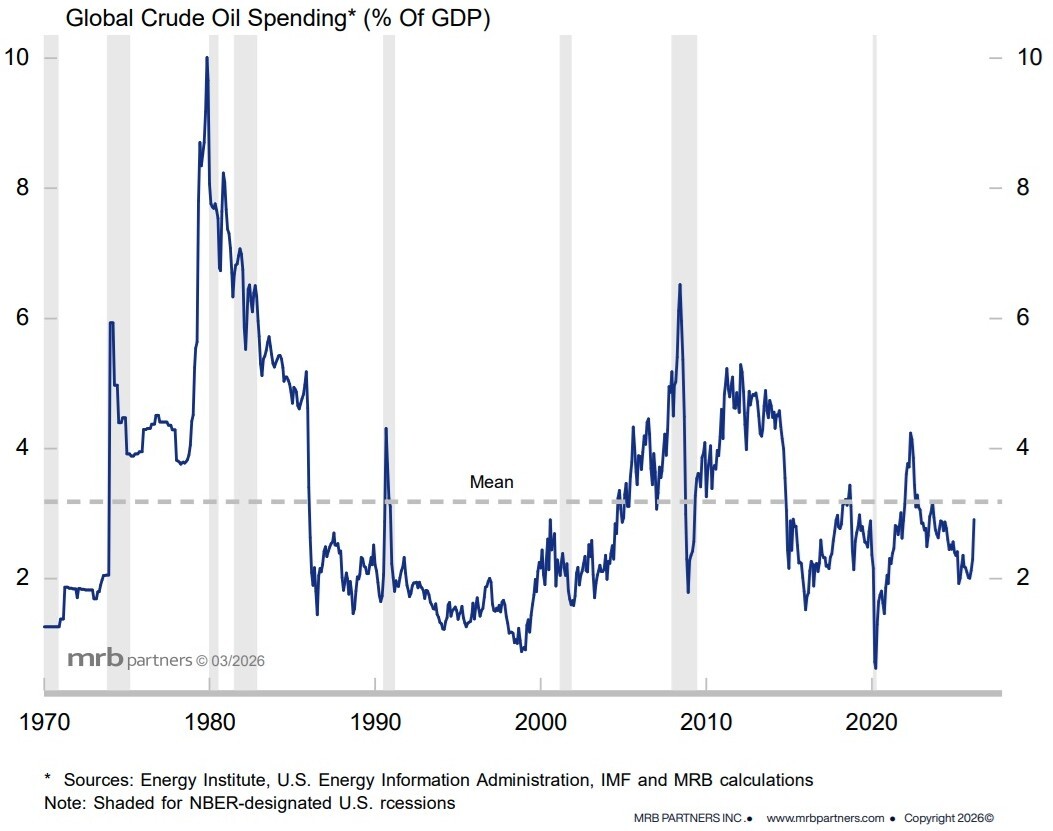

That said, the economy today is not nearly as reliant on low energy prices as it used to be. Technological advancements (fuel efficient vehicles, heat pumps, LED lighting, better insulation, etc.) have allowed us to produce more while using less. Coming into the war, oil prices were hovering around $60/bbl and spending on crude oil represented ~2% of global GDP. If prices average $100/bbl going forward, then spending on crude oil would be around 3.3%, which is in-line with the 50-year average.

INFLATION WILL SPOIL THE PARTY

If the war de-escalates, then we expect the positive economic trends that were in place heading into the war will resume. Specifically, economic growth and global trade were reaccelerating. That was due in part to central banks cutting rates these past few years. Lower borrowing costs leaves more money in consumers and corporations pockets, which they can use for spending or reinvestment respectively. Governments have been running large and growing deficits, further boosting growth. As a result, after a temporary slowdown from the war, we expect growth to re-accelerate.

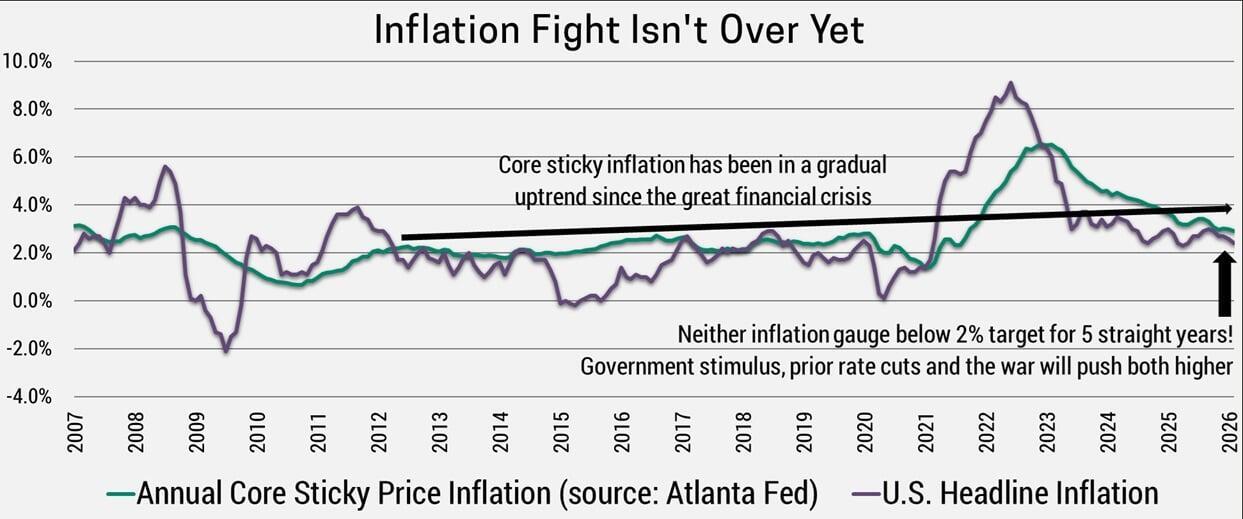

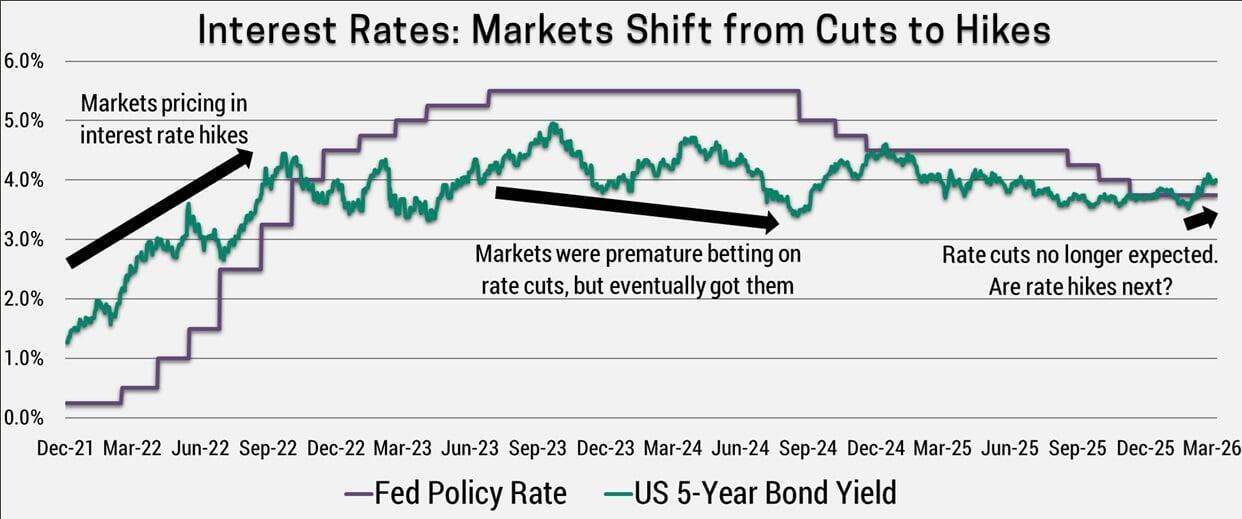

The real problem for investors is inflation; a topic we’ve covered many times before. We believe it will be structurally higher going forward, and higher energy prices only reinforces this view. Whenever you value an investment, you’re projecting their future earnings and cash flows, then discounting them back to the present. As inflation pushes interest rates up, investors must discount future earnings more heavily, arriving at a lower valuation. This effect is most significant for assets that derive more of the value from the long-term, like growth stocks and long-term bonds.

In short, we expect a resilient economy to produce higher earnings, but this will be partially offset by lower valuations due to higher inflation and interest rates.

PORTFOLIO STRATEGY

Given the significant risks and limited potential upside in equity markets, we recently deployed the proceeds from our U.S. equity sale into local-currency emerging market debt. This is paying a 5% yield and gives us exposure to emerging currencies which are cheap when measured in terms of purchasing power parity. If the war de-escalates and global trade/growth recover, emerging market currencies should appreciate, further boosting returns.

Our preference for Europe, Japan and emerging market stocks remains intact. The war has had disproportionately negative consequences for these regions because they are net energy importers and more reliant on global trade, which has been temporarily disrupted. The U.S. has held up better, as they became a net energy exporter in 2019 so are less exposed to higher oil prices.

International and emerging markets dramatically outperformed in 2025, so some of last month's underperformance could be investors taking profit. We believe this is temporary. While the short-term impact does relatively favour the U.S., the long-term impact of higher energy prices is higher inflation. As we’ve spoken about at-length in prior newsletters, the U.S. has more underlying inflation pressure and this will exacerbate the problem. As a result, we believe this war provides an opportunity for investors to diversify out of the U.S. Since we already expected U.S. underperformance and higher inflation, we are comfortable with our current portfolio positioning.